Understanding the savings vs checking accounts difference is not just a matter of basic banking knowledge it is a critical component of strategic financial management. For professionals, executives, and financial planners, these two account types serve distinct but complementary roles in managing liquidity, optimizing returns, and maintaining financial discipline.

A checking account is primarily designed to facilitate high-frequency transactions, enabling seamless payments, withdrawals, and day-to-day financial operations. In contrast, a savings account focuses on preserving funds while generating modest returns, making it an essential tool for building financial stability and managing surplus capital.

This guide provides a deeper, more analytical breakdown of savings vs checking accounts, introduces a quick comparison table, expands on debit card functionality, and offers detailed strategic and advanced financial insights.

What Is a Checking Account?

A checking account is a highly liquid deposit account designed for frequent transactions and operational financial activities. It is the backbone of daily financial execution.

Key Functional Features

- Unlimited or high transaction volume

- Real-time access to funds

- Integration with payment systems

- Overdraft capabilities (subject to bank policies)

Debit Card Integration

A defining feature of checking accounts is the debit card, which provides:

- Instant payment processing at POS terminals

- ATM withdrawals for cash access

- Online and international transactions

- Contactless payments (NFC-enabled cards)

- Spending tracking through banking apps

Professional Insight:

Debit cards linked to checking accounts enhance transactional efficiency, but they also require:

- Strong fraud monitoring

- Spending controls

- Reconciliation processes for businesses

What Is a Savings Account?

A savings account is structured for capital preservation and gradual financial growth. It is less about transactions and more about strategic fund allocation.

Core Features

- Interest-bearing deposits

- Limited withdrawals

- Higher security for stored funds

- Encouragement of saving discipline

Debit Card Access in Savings Accounts

While some savings accounts offer debit cards:

- They typically come with restricted usage

- Limited number of withdrawals per month

- Not ideal for frequent payments

Professional Insight:

Using debit cards with savings accounts should be restricted to controlled access, ensuring that funds remain preserved.

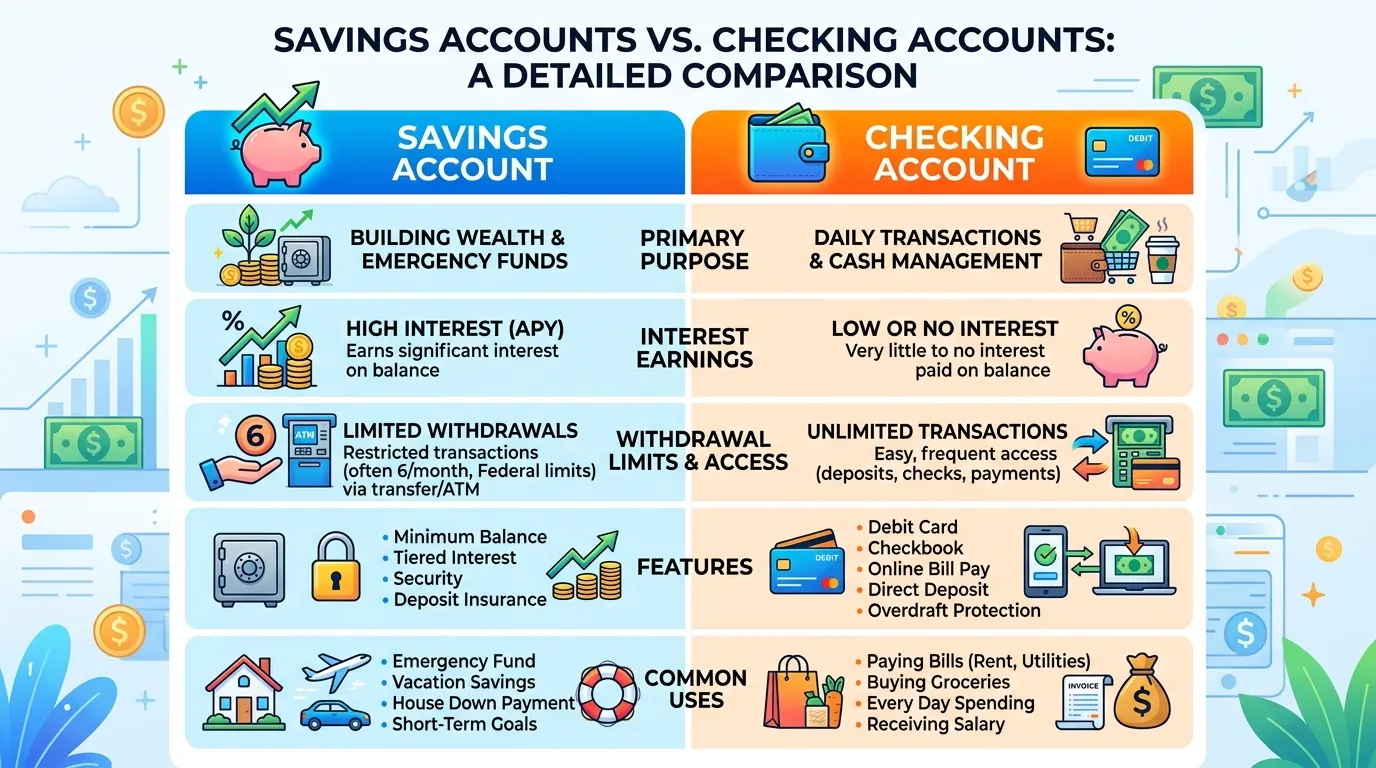

Quick Comparison Table (Checking vs Savings Account)

| Feature | Checking Account | Savings Account |

| Primary Purpose | Daily transactions | Saving and wealth accumulation |

| Liquidity | Very high | Moderate |

| Interest Earnings | None or very low | Moderate (varies by bank) |

| Debit Card Usage | Extensive, unrestricted | Limited or restricted |

| Transaction Limits | Unlimited or high | Limited withdrawals |

| Fees | Higher (overdraft, maintenance) | Lower (conditional) |

| Best Use Case | Expenses, payments, operations | Emergency funds, reserves |

Detailed Differences Between Savings and Checking Accounts

Below is a deep, professional-level comparison of the difference between savings and checking accounts, expanding into 10 detailed dimensions similar to the earlier analytical style.

1. Purpose and Financial Role

The most fundamental distinction lies in intended financial purpose.

- Checking accounts are designed for transactional efficiency, supporting daily inflows and outflows such as bill payments, payroll, and operational expenses.

- Savings accounts are structured for capital preservation and accumulation, acting as a repository for surplus funds.

Professional Insight:

Checking = operational engine

Savings = financial reserve layer

2. Liquidity and Accessibility

Liquidity refers to how quickly and easily funds can be accessed.

- Checking accounts offer immediate and unrestricted access to funds.

- Savings accounts provide controlled access, often with withdrawal limitations.

Why it matters:

High liquidity is essential for managing cash flow volatility, while limited access in savings accounts helps enforce financial discipline.

3. Interest Rates and Earnings Potential

A critical financial difference is return generation.

- Checking accounts generally provide negligible or zero interest.

- Savings accounts offer interest income, though rates vary based on market conditions and banking institutions.

Advanced View:

Keeping excess funds in checking accounts results in opportunity cost, especially for professionals managing significant balances.

4. Transaction Volume and Behavior

Transaction capacity significantly differentiates both accounts.

- Checking accounts support frequent and high-volume transactions without restriction.

- Savings accounts impose transaction limits, making them unsuitable for operational use.

Professional Angle:

This difference directly influences spending behavior and financial control mechanisms.

5. Debit Card Functionality and Usage

Debit cards play a central role in modern banking.

- Checking accounts come with fully functional debit cards enabling:

- POS payments

- ATM withdrawals

- Online and international transactions

- Savings accounts may offer debit cards, but with:

- Restricted usage limits

- Lower transaction thresholds

A Deeper Comparison

| Feature | Checking Debit Card | Savings Debit Card |

| Daily Transactions | Unlimited | Restricted |

| ATM Withdrawals | Frequent | Limited |

| Online Payments | Fully enabled | Often limited |

| Risk Exposure | Higher | Lower |

Strategic Takeaway:

- Use checking debit cards for operational spending

- Avoid frequent use of savings debit cards to maintain financial discipline

6. Fee Structures and Cost Implications

Cost efficiency varies between account types.

- Checking accounts often include:

- Monthly maintenance fees

- Overdraft penalties

- ATM usage charges

- Savings accounts typically:

- Have lower fees

- Require minimum balances to avoid penalties

Professional Tip:

Evaluate accounts based on net financial impact, not just visible fees.

7. Risk Exposure and Security

Risk differs due to accessibility levels.

- Checking accounts carry higher exposure to fraud and unauthorized transactions due to frequent usage.

- Savings accounts offer enhanced security by limiting transactional activity.

Management Insight:

Segregating funds between both accounts reduces financial vulnerability.

8. Cash Flow Management Role

Each account serves a distinct role in cash flow architecture.

- Checking accounts manage active cash flow cycles

- Savings accounts act as buffer reserves

Professional Application:

Maintaining this separation ensures:

- Smooth operations

- Financial stability during disruptions

9. Behavioral and Psychological Impact

Financial tools influence user behavior.

- Checking accounts encourage frequent spending and financial fluidity

- Savings accounts promote delayed gratification and disciplined saving

Behavioral Finance Insight:

Limiting access to funds (via savings accounts) can significantly improve long-term financial outcomes.

10. Strategic Financial Positioning

From a high-level perspective, both accounts serve different roles in a financial ecosystem.

- Checking accounts = short-term financial execution tool

- Savings accounts = short-to-medium-term capital holding instrument

Advanced Perspective:

Professionals should align account usage with:

- Liquidity needs

- Risk tolerance

- Financial goals

Strategic Financial Management (Savings vs Checking Accounts)

Professionals should adopt a multi-layered financial strategy using both account types.

1. Tiered Liquidity Framework

Divide funds into:

- Tier 1 (Checking Account): Immediate expenses

- Tier 2 (Savings Account): Emergency reserves

- Tier 3 (Investments): Long-term wealth generation

This ensures:

- Operational efficiency

- Risk mitigation

- Capital optimization

2. Automated Fund Allocation

Set up:

- Automatic transfers from checking to savings

- Percentage-based income allocation

Benefits:

- Eliminates manual decision-making

- Builds consistent saving habits

3. Cash Flow Optimization

Maintain only necessary funds in checking accounts and move surplus to savings:

- Reduces idle capital

- Improves overall financial efficiency

4. Risk Segmentation

Separating funds across accounts protects against:

- Fraud

- Unauthorized transactions

- Financial mismanagement

5. Emergency Buffer Strategy

Savings accounts should hold:

- 3–6 months of expenses (minimum benchmark)

For professionals with variable income:

- Increase buffer to 6–12 months

Advanced Considerations for Professionals

1. Opportunity Cost Analysis

Idle funds in checking accounts generate zero or minimal return. Professionals should:

- Quantify lost interest

- Compare with alternative savings instruments

2. Inflation and Real Return

Savings accounts offer nominal returns, but real returns depend on inflation.

- If inflation > interest rate → loss of purchasing power

- Use savings accounts for short-term holding, not long-term growth

3. Behavioral Finance Perspective

Checking accounts encourage spending behavior due to:

- Easy accessibility

- Debit card usage

Savings accounts enforce:

- Psychological barriers to spending

4. Digital Banking and Fintech Integration

Modern financial tools offer:

- Smart budgeting dashboards

- Automated saving rules

- Real-time alerts

Professionals should leverage:

- Multi-account management platforms

- AI-driven financial insights

5. Business vs Personal Account Strategy

For business professionals:

- Checking account: operational transactions

- Savings account: retained earnings and tax reserves

Separation improves:

- Accounting clarity

- Financial reporting accuracy

FAQs: Difference Between Savings and Checking Accounts

1. What is the main difference between savings and checking accounts?

The main difference is their purpose: a checking account is used for daily transactions, while a savings account is designed for storing money and earning interest over time.

2. Which account is better for daily expenses?

A checking account is better for daily expenses because it allows frequent deposits, withdrawals, and payments using debit cards, online banking, and cheques.

3. Can I use a savings account like a checking account?

Technically yes, but it is not recommended. Savings accounts usually have withdrawal limits and restrictions, making them unsuitable for frequent transactions.

4. Do savings accounts earn interest?

Yes, savings accounts typically earn interest on deposited funds, while checking accounts usually offer little or no interest.

5. Can I get a debit card with both accounts?

Yes, most banks provide debit cards for both savings and checking accounts, but checking account debit cards usually have fewer restrictions.

6. Which account is safer for storing money?

A savings account is generally safer for storing money because it is less frequently used, reducing the risk of overspending or unauthorized transactions.

7. Are there transaction limits in checking accounts?

Checking accounts usually have no strict transaction limits, making them ideal for frequent payments and business operations.

8. Why do people need both savings and checking accounts?

People use both accounts to manage money efficiently—checking for spending and savings for storing and growing funds.

9. Which account is better for emergencies?

A savings account is better for emergencies because it helps build a financial cushion that is not easily accessed for daily spending.

10. Can businesses use savings and checking accounts?

Yes, businesses commonly use checking accounts for operations and savings accounts for reserves or future investments, improving cash flow management.

Conclusion

The difference between savings and checking accounts lies in their fundamental financial roles—transactional efficiency vs capital preservation. For professionals, the goal is not to choose one over the other but to strategically integrate both.

By leveraging checking accounts for daily operations and savings accounts for reserves, professionals can:

- Optimize liquidity

- Minimize financial risk

- Enhance capital efficiency

A well-structured financial system built on these principles enables smarter decision-making and long-term financial stability.

Summary Insight for Savings vs Checking Accounts

The difference between savings and checking accounts is best understood as a balance between:

- Liquidity vs Control

- Spending vs Saving

- Access vs Growth

For professionals, integrating both accounts into a structured financial strategy is essential for optimizing cash flow, minimizing risk, and enhancing overall financial performance.

I am content creator and comparison blogger focused on analyzing key differences between terms, concepts, and ideas to deliver accurate, easy-to-understand information. So I decided to create a platform where these differences are explained in the simplest way possible.